BRSR Reporting: Bridging Critical Challenges and Information Gaps for Businesses

Abstract

Amid evolving ESG and sustainable reporting frameworks from voluntary to mandatory, corporate regimes are facing uphill in the adoption of sustainable practices in their operations. BRSR reporting, recently developed by SEBI in 2021 has been amended twice and made comprehensive over the last 3 years. However, under this new mandatory reporting regime, companies face challenges in their implementation and information gaps in their reporting. This article delves deeper to analyze the common mistakes that textile companies are making while developing the report, guiding on how to write answers while focusing on the most important indicators, and how to reduce the vagueness in the answers by simply understanding the use of ‘Nil’,‘-’, ‘0’ and point out the areas of improvement. As good reporting translates into good ratings, companies need to overcome new challenges of lack of knowledge among their untrained staff and increasingly adopt the use of services of third parties such as GreenStitch which specializes in “carbon accounting” and “Fashion ESG” reporting.

GRI established a unified framework for ESG reporting globally in 1997, though it was voluntary. Over the years, many regulations such as the GHG protocol in 1998, the Carbon Disclosure Project in 2002, and SASB standards in 2011 have been introduced due to the increased demand for ESG reporting by the regulators. Further, to meet the demands of the investors for the standardization and comparability in the ESG and sustainability initiatives of the organizations led this landscape for a transition from voluntary to mandatory regime. The myriad global and country-specific regulations such as TFCD, SEC Climate Disclosures, SFDR, and EU CSRD have been driving other countries to adopt mandatory regimes to make their domestic companies competitive in the investment market. In a larger context, such frameworks are driven by the global need to uphold sustainability and hold companies accountable for transparently integrating ESG responsibilities into their operations and annual reports. Walking on the same lines, India also has developed its own mandatory comprehensive sustainability reporting framework, based on the lines of GRI.

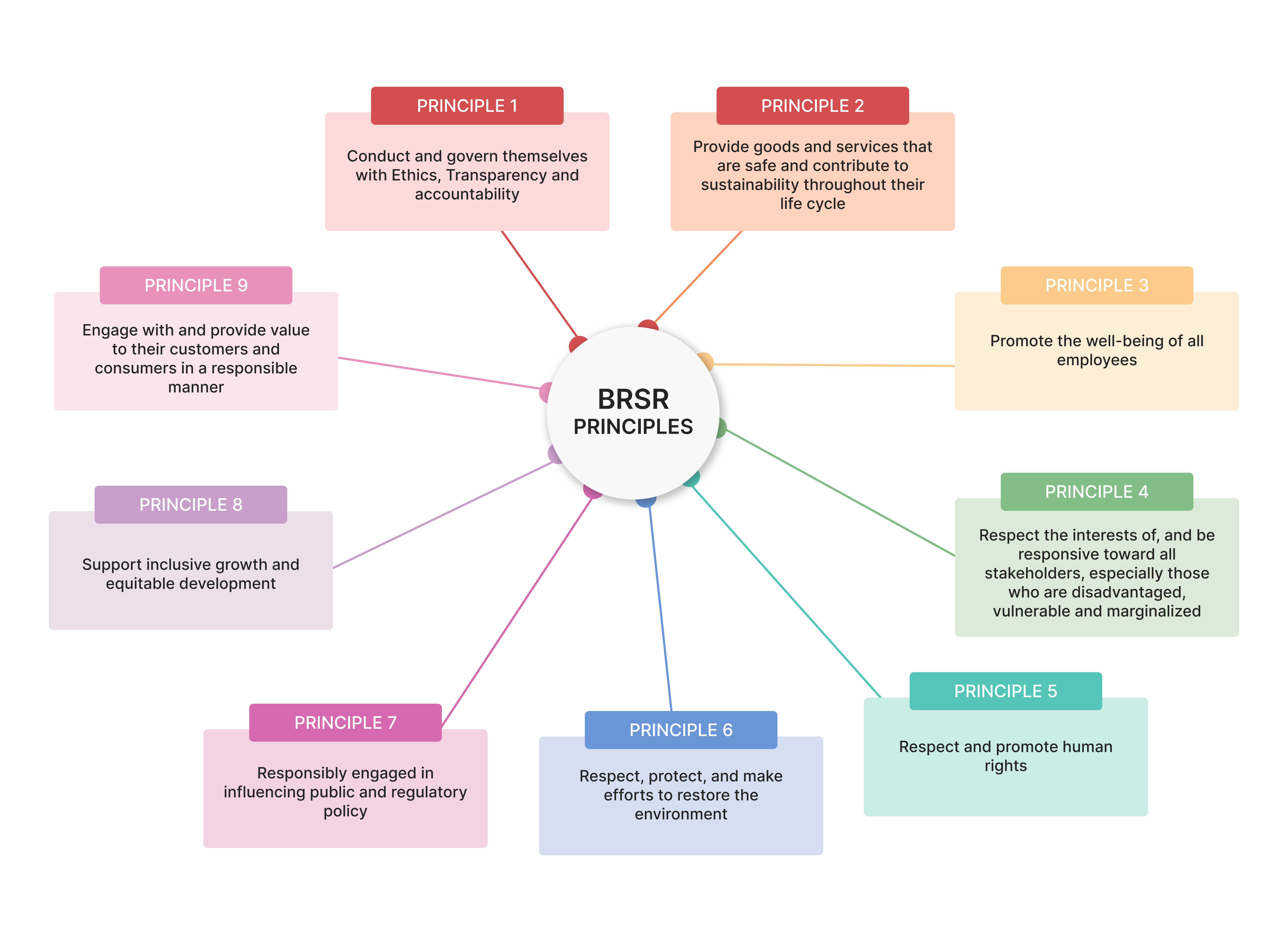

SEBI introduced the Business Responsibility and Sustainability Reporting (BRSR) framework in 2021 (format in Annexure 1), which is an extensive version of Business Responsibility Reporting (BRR). This framework mandates the top 1000 listed companies (by market capitalization) to disclose their ESG performance, reflecting their commitment to responsible business practices. This non-financial and qualitative reporting aims to standardize ESG reporting is structured around nine National Guidelines on Responsible Business Conduct (NGRBC) principles and includes essential and leadership (voluntary) indicators. The framework also offers a 'BRSR Lite' version for entities new to sustainability reporting, featuring fewer indicators. To bolster the BRSR framework and improve the trustworthiness of ESG disclosures, SEBI introduced the BRSR Core for the top 150 companies in 2023 which would be later increased to the top 1000 in FY’27 (250 by FY’25, 500 by FY’26). These companies are mandated to report their performance on nine ESG attributes in their value chain, each with specific key performance indicators. BRSR Core imposes stricter requirements than BRSR, as its disclosures necessitate reasonable assurance. This means a third party (like an auditor) affirms the accuracy of the information, ensuring reliability and credibility and boosting investor trust.

Why is it important?

BRSR framework serves a dual purpose, it establishes a standardized format for ESG disclosures and offers guidance through its set of indicators. Standardization of ESG reporting brings uniformity and comprehensiveness to the reporting which helps investors compare performance1 across peers, industries and even complementing sectors. This has reduced the autonomy of the companies in reporting the indicators of their choice and demand details of the actions and initiatives they have taken for the global good, instilling accountability in them. Further, this framework acts as a roadmap for setting the internal processes right as it reduces the lack of information in the organizations. The framework steers the company by mentioning the initiatives/actions one company should undertake and asks for progress on the same. Following the BRSR framework diligently, the companies can look for lower costs of capital, improved stocks & valuations, efficient operational practices, and reputation gains in the mid to long term.

It is also a strategic and multifaceted tool for investors offering capabilities of data analysis, risk management, performance evaluation, engagement, and decision-making. Investors can track improvements in ESG metrics over time and identify potential risks such as regulatory non-compliance, supply chain disruptions, reputational damage, or climate-related impacts. Alignment with global standards has made it easier for investors to make inter-country investment decisions. The emergence of new ESG regulations such as the EU’s Carbon Border Adjustment Mechanism (CBAM) and the SEC's climate disclosure rule underscores the profound impact on Asia Pacific companies should similar regulations not be mandated within the region, particularly in India. Thus, this swift introduction of ESG framework in India is a proactive step aligned with dynamic changes unfolding on a global scale and helps make domestic companies competitive in the global market amid the corporate landscape of sustainability and transparency.

Major reporting gaps in BRSR by companies

There are 178 textile companies in the top 2000 companies by market capitalization listed on the National Stock Exchange. These companies are engaged in spinning, fiber production, fabric production, technical textiles, home apparel, footwear, etc. There are 80+ textile companies in the top 1000 by market capitalization that are required to maintain a mandatory BRSR report. However, after analyzing a few reports, common mistakes that companies make while developing the report include: ignoring leadership indicators, not quantifying the objectives, inputs, and outputs, being unable to include even the smallest of initiatives, and giving a general broader perspective rather than specific to the organization.

Apart from this, discrepancies have been observed section-wise in the BRSR reporting of the companies in the textile sector. As per survey, Only 26% of the information was available in the section on Principle-Disclosure, 46% in Management & Process Disclosures, and 54% in the section on General Information. However, these numbers were higher for IT, banking, financial, services and insurance, and the chemical sector companies. The section that recorded the least amount of information is Principle 8 of inclusive growth while Principle 4 (Marginalised Stakeholders) and Principle 7 (Regulatory Policies) recorded the highest amount of information.

Ignoring leadership indicators in BRSR reporting: Many companies neglect the leadership indicators in their BRSR due to their voluntary nature. This is observed in terms of not earnestly answering the questions or entirely skipping up the indicators. For instance, marking information on training programs as ‘Nil’. Further, under Principle 6 questions on Scope 3 emissions are answered as ‘Nil’. Questions on water discharge in different water streams are marked 0. Most of the questions about value chain partners have even been marked as Not Applicable or Nil. Missing such direct crucial environment-related questions can result in an incomplete and potentially misleading report and diminish investor confidence, as it suggests a reluctance to fully engage with and be accountable for their ESG responsibilities.

Failure to Quantify Objectives, inputs, and Outputs: When objectives and outputs are described qualitatively, they can seem vague and unconvincing to investors. For instance, instead of stating "increase in sustainable sourcing of raw materials," support this claim with a specific percentage of increase. Similarly, if the goal is to increase reliance on renewable energy, specify the intended capacity to be achieved, the timeframe, and the steps already taken towards this goal. On similar lines, a specific number of training programs conducted would help in gauging the coverage of employees trained and even how much value chain partners have been covered. Providing concrete data makes the objectives clear and measurable, enhancing their credibility.

Categorization wherever possible: Use categories in questions wherever possible. For instance, in the “A brief on types of customers” question, companies can use categories such as wholesalers, retailers, brands, and exporters. Such categories can be supplemented with the brief. This breakup can be further classified as per the reach of the company. This provides clear information on the company’s customer base.

Improper Framing of Material Issues and Explanations: An analysis of several BRSR reports reveals that material issues are often not identified correctly and in tandem with sustainability and climate change. For instance, instead of using the term "Air emissions," it is more appropriate to specify "GHG emissions." Similarly, broad terms like "Climate change strategy" can be too vague and lead investors in multiple directions. To avoid this, it is important to mention specific issues such as wastewater management, reduction in GHG emissions, and land degradation, along with the company’s specific mitigation approaches. Avoid general statements like “taking concerted efforts in anticipating the effects of climate change.” Instead, provide concrete examples, such as ‘installing LED lights in offices to save energy’ or ‘installing wastewater management plants in all production units’.

Data recording gaps: Some environmental metrics such as water consumption, waste generation, or e-waste certificates, fuel consumption, energy consumption, waste storage and disposal, and even impact made through CSR activities are pertinent in BRSR reporting. Data gaps in these indicators often omit the necessary quantitative information and do not happen to make a necessary impression on the investors.

Discrepancies in value chain data reporting: The questions relating to value chain partners such as awareness programs conducted for value chain partners on any of the Principles during the financial year; Details on health and safety practices assessment of value chain partners; Provide details of any corrective actions taken or underway to address significant risks/concerns arising from such assessments above under the Principle 1, 3, and 6 are either marked as ‘Nil’ or ‘-’ or ‘NA’ or not feasible. Even if some of the questions are answered then concrete steps and measures are not mentioned. Thus, this raises the vagueness and questions the credibility of the report. Further, it shows the non-commitment of the company towards its value chains.

Vagueness due to ‘-’ or ‘Nil’: At various places, companies have used ‘-’ or ‘Nil’ which creates a problem in interpreting the answer. For example, mentioning ‘-’ in ‘the number of employees differently-abled’ does not give a good impression. Since this is a quantitative data point, thus instead of writing ‘-’ it should be 0. Similarly, this problem persists in the ‘number of complaints registered’. If there are ‘no complaints’ the ‘Nil or ‘0 should be used and if the data was not calculated then "-" should be used. This gives a clearer idea. It is important to understand the nature of a question as qualitative and quantitative before writing the answers.

Strategically focussing on ‘important indicators’: Companies should focus on detailing the questions relating to indicators that global ranking indexes such as Moody’s, MSCI, S&P, etc focus on. For instance, MSCI’s ESG Ratings2 for textile companies which provide an assessment of the long-term resilience of companies to ESG issues focus on indicators such as environmental factors (26.5%) like raw material sourcing, product carbon footprint, social indicators (37%) such as labor management, chemical safety, supply chain labor standards and governance (36.6%). Questions relating to these indicators in BRSR format should be answered with high integrity and diligently to improve the rating in this particular index.

Filling incorrect information: For instance, companies are, in question relating to the identification of material issues of the organization in Section A, column fifth ‘in case of risk, approach to adapt or mitigate’ is to be filled only if the identified issue is categorized as ‘risk’. However, few companies are filling this column even if the identified issue is an ‘opportunity’ which comes across as unnecessary information and makes the whole answer vague.

Challenges for businesses in developing BRSR reports

Complexities of data collection and consolidation: Data management is an arduous aspect of BRSR reporting in large companies. Undigitized data, fragmented data points, and the onerous task of compiling and harmonizing data from different formats and sizes are some of the complexities that large companies face. Moreover, due to the fragmentation of units of production and services, consolidating data on various themes such as energy and electricity consumption, waste usage, waste production, and recycling of each unit and then compiling them is a tedious and financially expansive task. Such processes are more draining for small companies without the necessary resources and personnel. Thus, turning towards automated AI software such as GreenStitch can help in calculating “Scope 1, 2 and 3 emissions” of organizations.

Increase in workload for staff: With no special team in place for sustainability in various companies, the workload of existing staff is bound to increase. Further, they have the pressure to upskill themselves to have the required knowledge for data collection and reporting in BRSR format. Further, companies also have to undertake additional training on ESG metrics for all employees since sometimes data collected can often be marred by inaccuracies or incompleteness without adequate knowledge.

Third-party evaluations: After the introduction of BRSR core which requires assurance from third-party evaluations, it has become pertinent for the companies to have third-party audits of the ESG metrics in their companies. Also, in BRSR format in Principle 6, it is given as a note to mention the audit conducted by external agencies. However, in existing cases most of the companies are not even undertaking internal evaluations of their ESG metrics, this number is especially high for small and medium companies. Thus, in the coming years, companies will not have the challenge to not only streamline their internal processes but also have sustainable audits of their operations.

Identifying the right personnel for each section of the BRSR reporting: The BRSR format is divided into three sections and the third section is based on nine principles with each principle classified based on essential and leadership indicators. If we closely examine the questions, it can be classified that answers are to be sought from the HR, product design, ESG, company secretary, finance, IT, sales, and marketing departments. For example, all the questions under Principle 3 fall in the arena of the HR department while Principle 4 falls in the forte of the Company secretary and ESG department. Classifying the reporting responsibilities will be a collective effort toward developing this report and reducing the hassle in terms of time and resources.

Conclusion

With the increasing mandatory ESG compliances and reporting frameworks, it has become imperative for textile companies to have experienced teams on sustainability. The functions of the team can include “carbon accounting”, data measuring and “fashion ESG” reporting, monitoring the information gaps, developing reports as per compliance, and developing strategies for a carbon-neutral entity. Establishing proper data collection strategies will help in avoiding reporting gaps in key environmental metrics. For this, timely awareness and training programs for employees can be conducted which are characterized by developed modules for BRSR reporting and framework. Training existing employees will reduce the burden of recruiting a special team.

Moreover, companies can look into the reports of companies such as Trident Ltd. and Page Industries which have developed the report in detail and mentioned specifics wherever required. Further, companies can even hire third parties having expertise in sustainability such as GreenStich which helps in calculating “Scope 1, 2 and 3 emissions” through “carbon accounting” and help in “fashion ESG” reporting through its ESG compliance module. The team of experts also provides guidance on various sustainability issues and help in supply chain decarbonisation by identifying the hotspots of carbon intensiveness. Greenstitch believes that good reporting translates into good ratings, thus it provides ESG reports tailored to the needs of the textile companies.

For more insights on the challenges faced by businesses in BRSR reporting; reach out to us at narendra@greenstitch.io

Annexure 1: Format for Business Responsibility and Sustainability Reporting

The format of BRSR is divided into three sections: General Disclosures, Management and process disclosures, and Principle-wise performance disclosures. The principal-wise disclosures include 68 essential and 38 leadership indicators where essential indicators are mandatory to report while leadership indicators are voluntary. After the introduction of BRSR Core, the structure of new format for BRSR is structured as follows:

Section

Number of Questions

Section A: General Disclosures

26

I. Details of Entity

15

II. Product/Services

2

III. Operations

2

IV. Employees

3

V. Holding, Subsidiary, and Associate Companies (including joint ventures)

1

VI. CSR Details

1

VII. Transparency and Disclosure Compliances

2

Section B: Management and Process Disclosures

12

Policy and management processes

6

Governance, leadership, and oversight

6

Section C: Principle-wise Disclosures

106

Principles

Essential

Leadership

Principle 1

9

2

11

Principle 2

4

4

8

Principle 3

15

6

21

Principle 4

2

3

5

Principle 5

11

4

16

Principle 6

11

4

16

Principle 7

11

4

16

Principle 8

11

4

16

Principle 9

11

4

16

68

38

Total Questions

144