CSRD, EU’s new directive for environmental reporting: Explained

Abstract

With the introduction of the “Corporate Sustainability Reporting Directive (CSRD)” in line with the Paris Agreement, it has become imperative for large companies and SMEs operating and listed in the EU to buckle up for more stringent, comprehensive, and mandatory non-financial sustainability reporting. This article explains which textile companies are going to be affected and what are the first steps for the companies new to sustainability reporting. EU has enlarged the ambit of CSRD, unlike its predecessor NFRD, by including MSMEs and companies from other countries operating in the EU. The introduction of novel ‘dual materiality assessment’ of ‘material’ topics and the unavailability of quality data has brought significant challenges to the table of textile companies hindering their ESG reporting progress. Read this article to know the steps to overcome these challenges and how an AI “carbon accounting” and reporting software such as Greenstitch will be helpful in their journey of ESG reporting.

To accelerate the shift towards net zero in European economies, the European Union (EU) initiated a series of green initiatives through the EU Green Deal1 and EU strategy for sustainable and circular textiles2 which aims to make textile products available in the EU economy durable, repairable, and recyclable by fostering the circular business models, profitable re-use and repair services, adoption of Digital Product Passport, tackle greenwashing and reduce overproduction and overconsumption of textiles. This strategy aims to complement the EU's climate, energy, transport, and taxation policies for reducing “carbon footprint and climate change” effects in Europe. Within these strategies, the “Corporate Sustainability Reporting Directive (CSRD)”, a non-financial reporting, emerged as an important legislation in 2023, that aims to bring consistency and comparability in the data relating to climate disclosures of the textile companies and help stakeholders such as customers, investors, financial market participants, policymakers, etc to evaluate the non-financial performance of the company and make better-informed decisions based on available sustainability data. This directive is an improved version of the Non-Financial Reporting Directive (NFRD), 2018 which was restricted to 11,500 public interest entities and listed companies in the European Union. NFRD gave flexibility to companies in terms of third-party audits which were optional for businesses. Companies had autonomy in reporting their sustainability information and this report could be submitted as part of their annual reports. However, owing to these loopholes, the EU has developed a more polished version of NFRD as CSRD which was introduced in January 2023.

Which companies have to report under the CSRD?

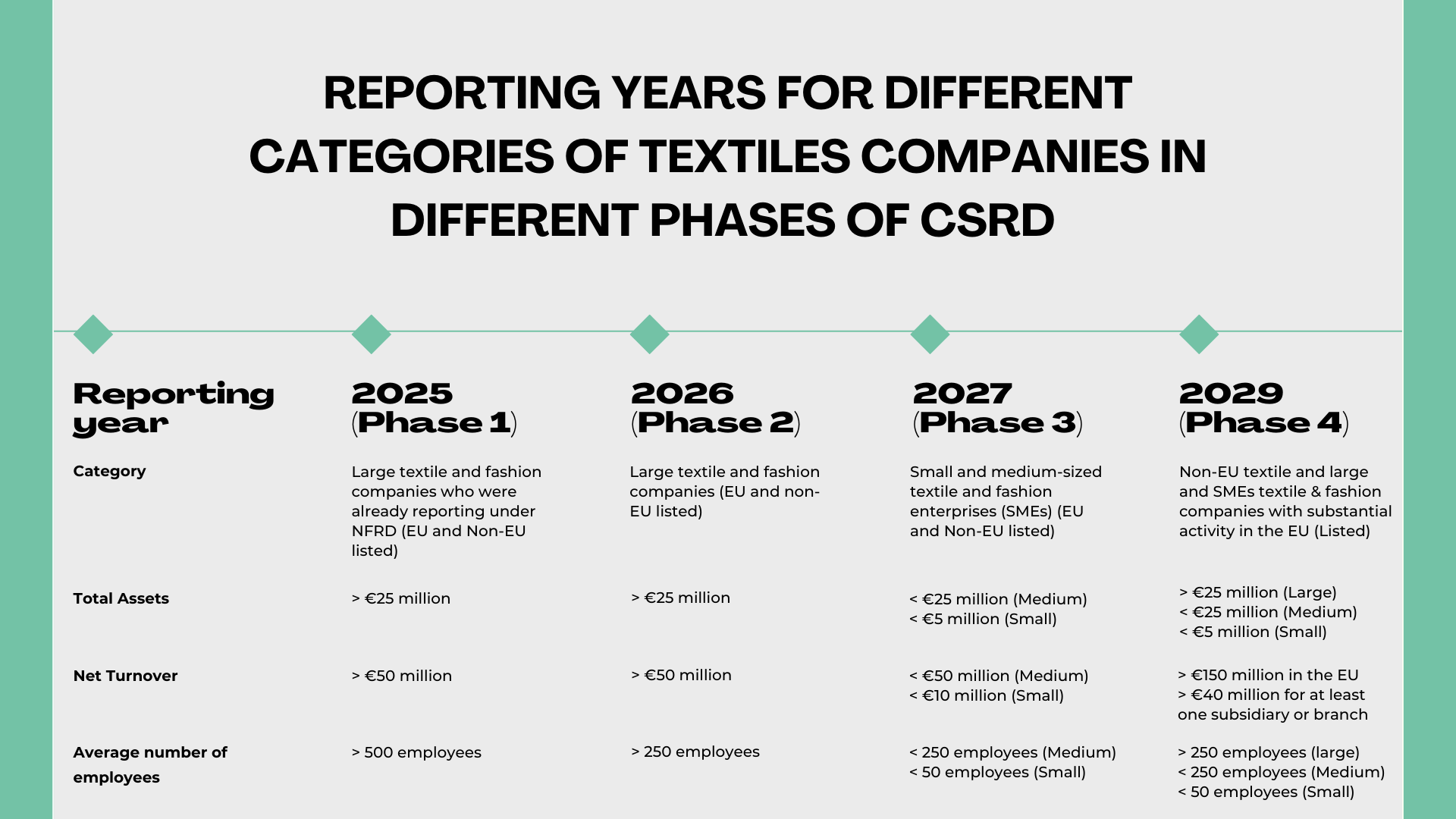

The Corporate Sustainability Reporting Directive (CSRD) expands its scope to almost all listed EU and non-EU textile and fashion companies (generating more than EUR 150 million) on the EU market regardless of the sector. The EU Textiles & Clothing industry currently includes 192,000 companies of which 89% are micro-enterprises, 9% are small enterprises, 2% are medium and 0.3% are large enterprises3. This legislation is set to affect more than 21,500 textile and fashion enterprises in the EU. Initially, it will be applicable to the listed companies having more than 500 employees and who were reporting under the old regime of NFRD, subsequently it will be extended to other large, medium, and small enterprises and non-EU listed enterprises. Micro enterprises are exempted from this directive for now. The sustainability reports for different categories of companies are to be submitted in 4 phases. The following infographic shows the timeline for different categories of enterprises to submit their initial report.

CSRD requirements for textile companies

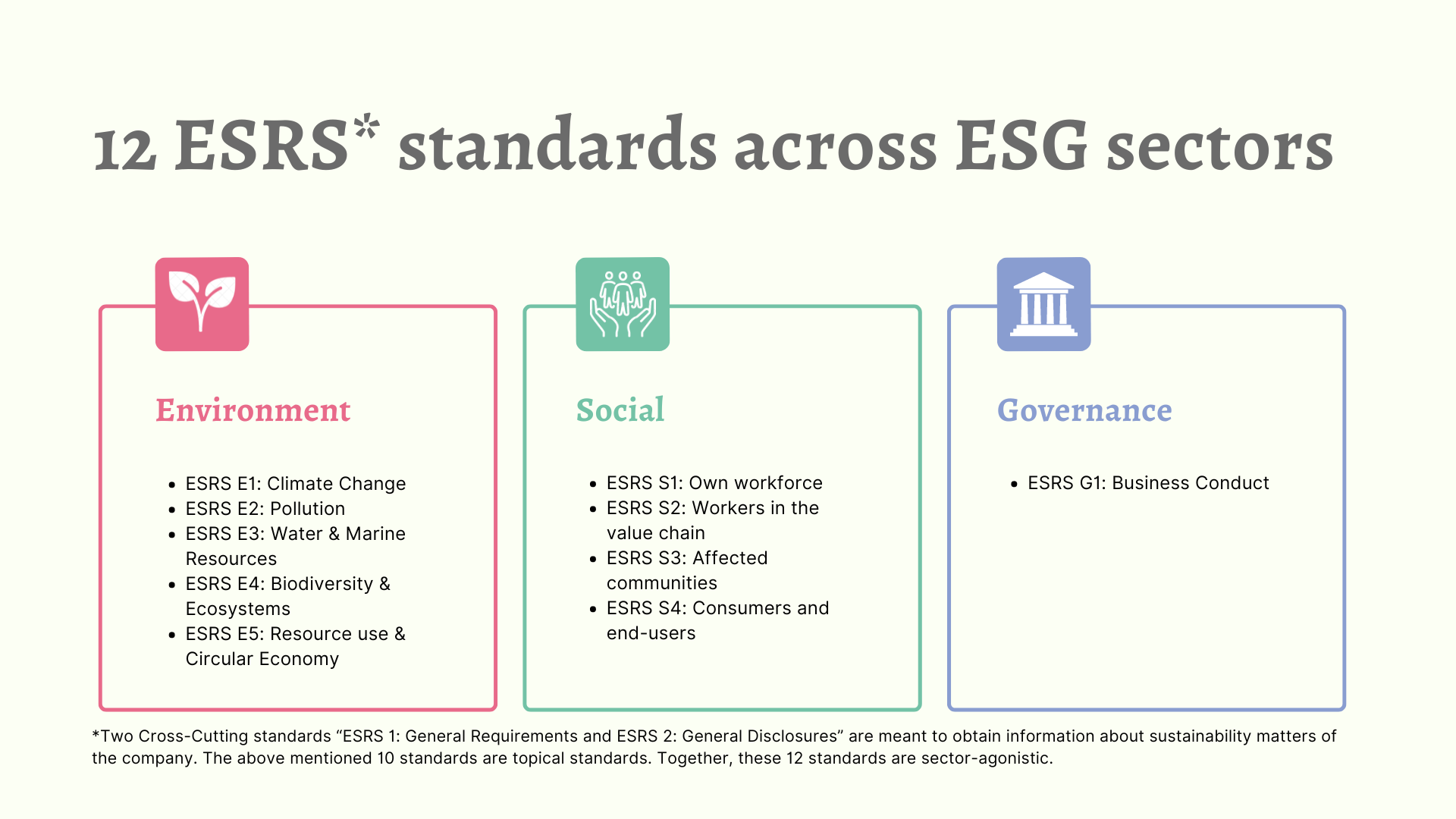

The textile companies have to report the information based on 12 European Sustainability Reporting Standards (ESRS)4 which seek information on environmental, social, and governance indicators, depicted below in the picture. Two of them General Requirements and General Disclosures are cross-cutting standards. These 12 standards are sector agonistic, meaning they shall apply to all companies regardless of their sector. However, sector-specific standards for textiles, accessories, footwear, and jewelry will be introduced in 2026,

Across these 12 standards, companies have to report on dual materiality comprising impact and financial materiality. Impact materiality shall focus on impacts, risks, and opportunities (IROs) that are likely to arise from the activities, business relationships, geographies, or other factors that the company undertakes and the impact it makes on natural, human, and social resources whereas financial materiality is concerned with the effects of sustainability matters on the company’s financial position, performance, cash flows, its access to finance or cost of capital over the short, medium or long-term.

ERSR 1 (General Requirements) sets general principles to be applied when reporting according to ESRS and does not itself set specific disclosure requirements. ESRS 2 (“General Disclosures”) specifies essential information to be disclosed irrespective of which sustainability matter is being considered. ESRS 2 is mandatory for all the textile companies under the CSRD scope. All the other standards and the individual disclosure requirements and data points within them are subject to a materiality assessment. This means that the company will report only relevant information and may omit the information in question that is not relevant (“material”) to its business model and activity. Further, suppose any organization feels that climate change is not material to its organization. In that case, such a textile company has to provide a detailed explanation of the conclusions of its materiality assessment about climate change.

Moreover, there will be a separate set of standards for textile SMEs, which will be less demanding than the full set of ESRS that the Commission has just adopted. For non-listed textile SMEs, the EU is developing a set of voluntary standards under which they can choose to report. Further, micro-enterprises are exempted from this regulation. Listed SMEs, including non-EU-listed SMEs, will have to publish their first sustainability statements in 2027. However, listed SMEs may opt out of the reporting requirements for another two years. The last possible date for a listed SME to start reporting is the financial year 2028, with the first sustainability statement published in 2029. In addition, standards for non-EU companies separate standards will be adopted.

How to start with the reporting under CSRD?

The ambiguity among textile organizations on how to start with CSRD reporting makes them vulnerable to this new legislation. This section details the two stages that are important before the development of a sustainability statement under CSRD. The first and foremost step is to conduct a double materiality assessment to identify the material topics and then conduct a gap analysis to identify the areas where data is not available. Based on this, a roadmap is to be constructed to fill in the gaps and move to the stage of ESRS reporting.

- Dual materiality assessment to identify IROs: This foundational task of double materiality assessment from the perspective of impact and will help in identifying the topics that are ‘material’ to a textile entity. For instance, these could be climate change, resource use, circular economy, and water and marine resources to name a few. It might be possible that not all ESG standards and indicators are material to the organization. Thus, after this assessment, the organization may omit several indicators but they have to justify their immateriality in cross-cutting standards of the sustainability statement. Further, they have to identify impacts, risks, and opportunities (IROs) in their materiality assessment on each material topic they have discovered. Identifying IROs calls for a thorough analysis of their value chain and operations which is possible with cross-departmental collaboration, close partnerships with supply chain partners, and maintaining meaningful communication with the stakeholders.

- Gap analysis and developing roadmap: After identifying the IROs and thus, their scope of reporting, the companies have to collect the data on the material topics. The foremost step in assessing the data gaps is the evaluation of data collection methods to understand their comprehensiveness. The company then has to assess the quality and quantity of “Scope 1, 2 and 3 emission” data, information on its workforce including benefits, policies, social protection measures, training and skill development, etc, and business conduct including business corporate strategy, conduct policies and culture discussion and promotion. The company has to identify the indicators where data collection is minimal and ensure it meets the stringent requirements of data accuracy as per CSRD. Further, the organization has to set up a specialized team or hire a third party such as Greenstitch which can facilitate data collection relating to environmental indicators across the supply chain of a textile company and help in reporting sustainability statements as per CSRD by integrating existing sustainability reports and databases.

- Sustainability Reporting: Finally, the company can start with the reporting of sustainability statements as per CSRD requirements. The ESRS framework is highly complex due to the extensive interconnections among its various indicators. These interconnections primarily arise from the cross-cutting standards that impact all other standards. Additionally, there are numerous interactions within the topical standards, which can differ from company to company. The ESRS also includes entity-specific disclosures, enabling companies to add extra information to address important issues (IROs) that the current standards might not adequately cover.

- Assurance from third-party: The CSRD mandates that a third party must audit and verify the sustainability information and data presented in the report. At first, compliance will involve the auditor offering limited assurance, which primarily depends on the organization's self-reported statements. However, the CSRD will escalate this requirement to reasonable assurance over the next three years. This means that the auditor will need to conduct a more thorough examination and gain a deeper understanding of the organization's operations, processes, and controls. This will provide investors and customers with the validated sustainability information to make a well-informed decision.

Challenges under CSRD

CSRD brings a lot of challenges to the table of textile companies due to its comprehensiveness and complex structure. CSRD has 12 standards covering 82 disclosure requirements — almost 1500 data points in total. The complexity of this nature compels companies to feel that there are a lot of issues that are to be considered beyond compliance under significant time pressure5, as the first report of CSRD is to be published in 2025 by the companies who are already under NFRD and the companies that are new to the sustainability reporting will have to furnish their first report in 2026. The following challenges that companies may face in the initial phase of implementation of CSRD:

- Unavailability of data: The companies must have information on 1500 points in total which is to be drawn from various verticals of the organization such as sustainability, risk, human resources (HR), environmental, health and safety (EHS), and legal. Further, they must collect information on different stakeholders such as employees, supply chain employees, and outside communities. The 2023 Verdantix global corporate survey of 400 sustainability leaders6 found that external collaboration with suppliers and customers is considered a critical challenge that firms face. If they are unable to collect the information on external stakeholders then companies have to specify the efforts made to collect the information, reasons for the inability thereof, and plans for the future to improve the same.

- Collecting data about their supply chain: Companies have to collaborate with their suppliers and partners to obtain supply chain CO2 emissions data for their CSRD reports. Helping supply chain partners in collecting carbon emission data will be essential for companies to position themselves ahead of the fast-approaching reporting timeframe of the CSRD. According to a survey, only 20% of EU-based respondents currently have—or expect to have—supply chain carbon emission data capable of meeting financial audit quality requirements by 2024.

- Ensuring high-quality data: Since CSRD mandates the companies to go through third-party audits in the first year of reporting moving to reasonable assurance within three years, it has become reasonable for companies to establish better governance and controls over sustainability data collection. This challenge will be more taxing for companies such as MSMEs who were till now not under the aegis of any ESG reporting mechanism. Additionally, the companies already preparing sustainability reports have to ensure that their data meets the rigorous standards of investor-grade data.

- Conducting a double materiality assessment: According to a survey by EY, it has found that only 8% of surveyed companies felt ready for the requirements of a full-fledged double materiality assessment. Many companies had approaches for materiality assessment as per voluntary frameworks GRI, SASB, and ISSB. However, they found double materiality assessment by CSRD completely novel. Following a rebuttable presumption principle, topics within the CSRD are assumed to be material unless proven otherwise, increasing the burden for firms. Additionally, this assessment will be subjected to assurance by third-party audits. Further, the companies operating and reporting at the global level have to find some intersection among many materiality approaches given by SEC, CSRD, and other frameworks to accommodate the differentiated regulatory and reporting requirements in different regions/economies.

Providing a forward-looking approach: Companies must formulate forward-looking plans for the short-term (1-5 years), medium-term (5-10 years) and long-term (10+ years). Information for these plans should be backed by scientific evidence whenever available. Further, they must detail the sustainability targets they have set for 2030 and 2050 in their CSRD reporting along with the progress made to achieve them.

Steps to overcome these challenges

38% of the 400 heads of sustainability surveyed said that they did not feel confident in their ability to deliver investor-grade, says survey7. This is owed to a lack of confidence arising from personnel capabilities, technological limitations, or organizational process complexities. Thus they either need to collaborate with third parties that offer specialized tailored solutions or to incorporate a specialized team for the evolving and emerging ESG reporting landscape.

Choosing the most appropriate digital solution: It is now imperative for textile companies to choose the most appropriate GHG tracking software like Greenstitch to help them calculate their “carbon footprint”, supply chain decarbonisation, product life cycle analysis, and traceability to ensure they meet the disclosures and data requirement under CSRD ESG reporting framework.

Assemble CSRD team: Given the complexities in CSRD reporting, it might be feasible for large companies to assemble a team having specialization in ESG reporting, frameworks, and regulations to reduce the burden of this additional work requirement on existing employees.

How Greenstitch can help in your sustainability reporting?

Greenstitch is a “carbon accounting software”, specially designed for textiles businesses, offering tailored solutions to your sustainability reporting issues. The software aims to reduce the data gaps with automation, decreasing manual efforts on the part of organizations. It specializes in the following areas:

- Carbon accounting Software: Greenstitch software is tailored especially for textile companies accounting for Scope 1, 2 and 3 emissions across their supply chains and processes such as yarn production, fiber production, ginning, spinning, weaving, dyeing, etc. It streamlines data management for organizations and suppliers while filling the data gaps with smart automation. It can integrate existing ERPs, inventory databases, and previous sustainability reports. The software is regularly updated with new standards introduced, methodologies, and conversion factors facilitating easier transition to new regulations.

- ESG reporting: Greenstitch has its own ESG Compliance module which helps it stay compliant with evolving global and regional sustainability regulations and collaborate with international teams to create comprehensive ESG and compliance reports tailored for the fashion industry, incorporating CSRD, BRSR, GRI, CDP, and SASB standards

- Product Life Cycle Analysis: With Greenstitch software, companies can conduct life cycle analysis of textile and fashion products from raw materials to the warehouse, and precisely measure their environmental impact, including scope 1, 2, and 3 emissions, water consumption, and land use footprints, even with minimal data.

- Supply Chain Decarbonisation: With Greenstitch, companies can quickly identify their hotspots and devise “ways to reduce carbon footprint”. They can foresee textile trends and get an overall snapshot of their organization against the industry.

References

- The European Green Deal

- EU Strategy for Sustainable and Circular Textiles

- Analysis of the EU Textile & Clothing industry external trade in 2023, Spring and Autum Report, Euratex 2023

- Commission Delegated Regulation (EU) 2023/2772 of 31 July 2023 supplementing Directive 2013/34/EU of the European Parliament and of the Council as regards sustainability reporting standards

- Corporate Sustainability Reporting Directive: the rush to get ready, EY, 2023

- Tackling the challenges of the CSRD: How to avoid the pitfalls and build readiness for CSRD and beyond, IBM, 2024

- Tackling the challenges of the CSRD: How to avoid the pitfalls and build readiness for CSRD and beyond, IBM, 2024