CBAM Transition: Opportunities and Challenges for the Textiles Sector

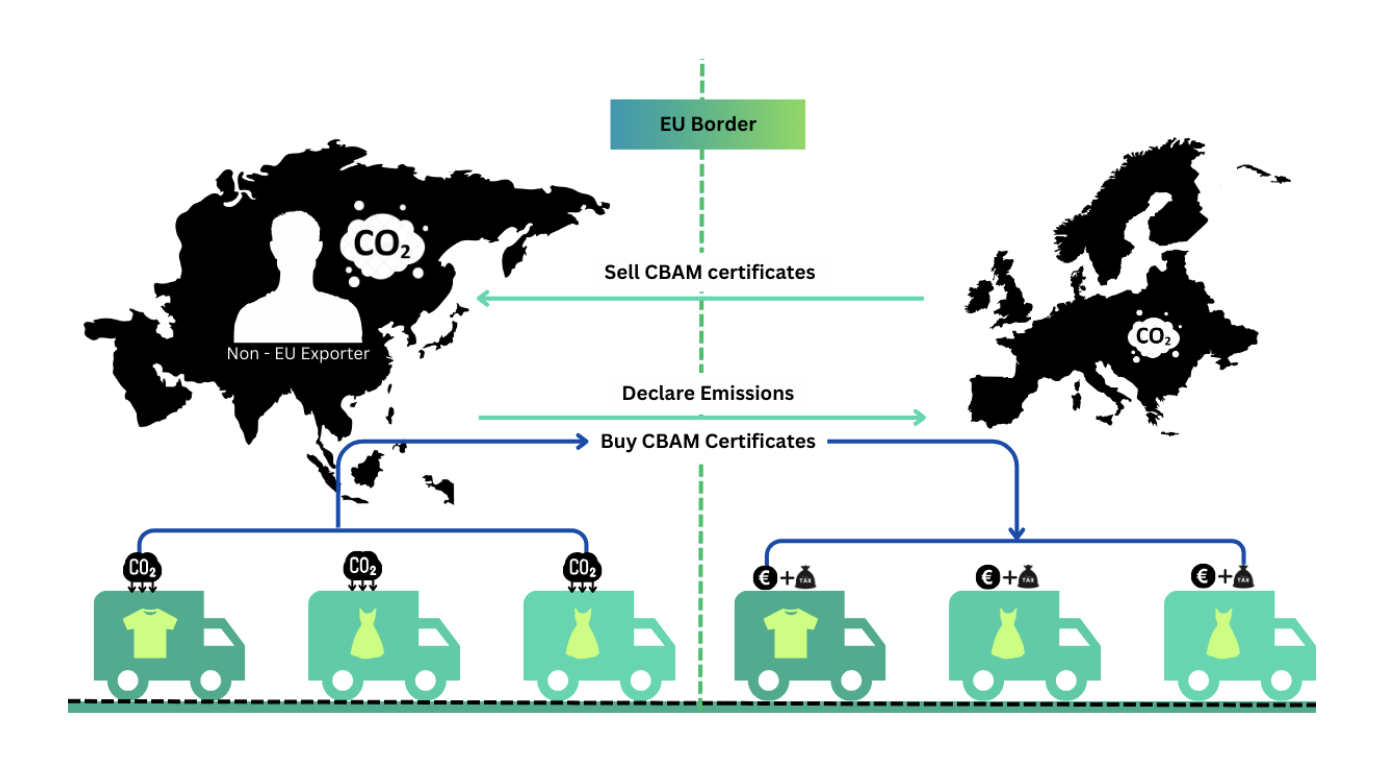

As you may be aware, the European Union (EU) has introduced a new carbon tool called the Carbon Border Adjustment Mechanism (CBAM) as part of its Fit for 55 agenda. This mechanism aims to tackle the risk of 'carbon leakages' by taxing high-risk emissions from imports from nations with less ambitious and stringent green standards.

In its transitional phase (2023-2026), the textiles sector is not part of this tax regime , however, given the high emissions involved in the manufacturing process of the textiles, it can come under its umbrella in the years following the definitive regime (2026 - 2034).

In this email, we will discuss the potential effects of CBAM on the textiles sector and how it may impact your business.

Potential Effects of CBAM on Textiles

The textile and garment sector is estimated to produce 10% of global carbon emissions of 1.7 billion tonnes per year. The EU, the world's largest importer of textiles, generated 121 million tonnes of emissions in 2020, making textiles one of the largest emitters of greenhouse gases in Europe. The fashion industry accounts for 10% to 15% of the total EU emissions. The European Parliament reports that there are 12.6 million tonnes of textile waste in the EU every year and only 1% of used clothes are recycled. It can be practicable for the EU to levy a carbon tax on textiles.

This would increase the cost of production and reduce the marginal profit for exporters in developing countries, which are the major suppliers to the EU. This green measure will make exports from outside the EU less competitive and impact the bilateral trade between the EU and the rest of the world. Other countries may counter this move and change the geopolitical dynamics of trade by implementing similar carbon tax regimes in their economies.

There will be opportunities for businesses in non-EU countries to re-evaluate their manufacturing and supply base footprints and move to greener procurement policies to reduce the emissions embedded in their product production and capture newer demands.

The carbon emissions from producing different articles of textiles depend on various factors such as the type of raw materials (cotton, polyester, wool, etc), technologies, amount of energy, and heat used in manufacturing processes. According to the report Fashion on Climate 2022 by McKinsey & Company, more than 70% of the GHG emissions come from upstream activities particularly energy-intensive raw material production (38%), yarn preparation (8%), fabric preparation (6%), wet processing (15%) and cut make trim (4%). The remaining 30% are generated by downstream activities such as transport (3%), retail operations (3%), usage (20%), and end-of-use (3%).

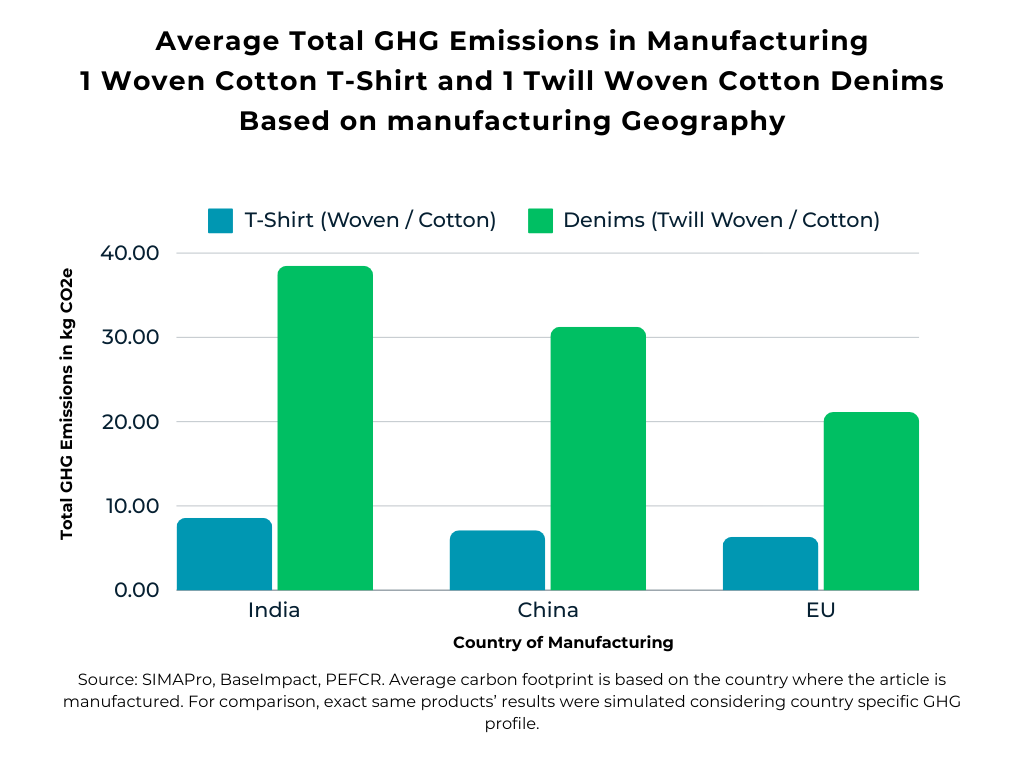

In developing countries such as India and China, carbon emissions embedded in the sub-processes of manufacturing textiles are higher than in the European Union. This can be illustrated in the figure below where the carbon emissions from producing one cotton jeans in India and China are 1.9 times and 1.5 times higher than in Europe respectively. Similarly, the carbon emissions in India for producing one cotton T-shirt are 1.3 times higher than in Europe. To reduce the gap in carbon intensities between domestic and foreign production, the EU has proposed the CBAM which incentivizes other nations to decarbonise their supply chains and production processes, if they want to enhance their bilateral trade with the EU countries.

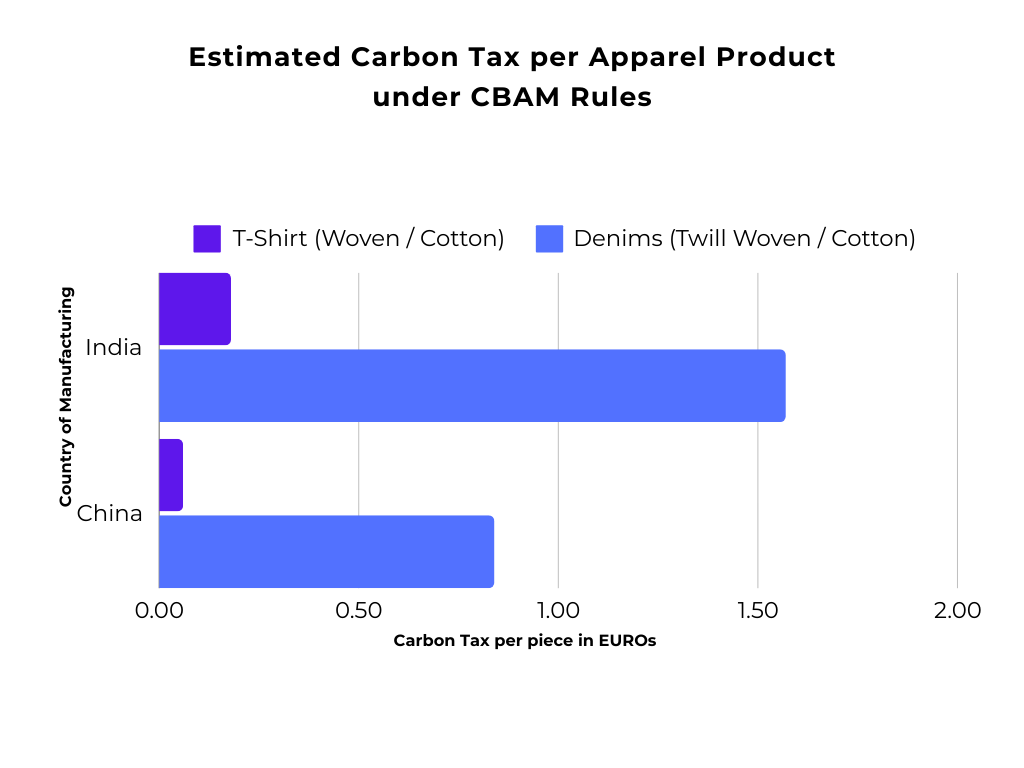

In Europe, the average price of a cotton T-shirt imported from India and China is €5.4 and €6.5 respectively. The average imported price for a pair of cotton jeans from India and China is €5 and €6.7 respectively. Based on the differences in carbon emissions in India and China from the production of both goods with Europe, exporters from India and China will pay an additional 3.4% and 0.9% of the imported price for exporting 1 kg of cotton T-shirts, respectively.

To export 1 kg of cotton jeans to Europe, India, and China are required to pay 31.8% and 13% more than the price of the dress imported. This is illustrated in the figure below:

Future Prospects

The EU may propose CBAM for textiles due to the huge carbon emissions generated by non-EU textile exporters. The top four textile exporters (Bangladesh, India, Turkey, and China) together emit 84% and 62% of GHG emissions from all non-EU cotton T-shirts and jeans exports respectively. Imports from Bangladesh and Turkey account for the highest percentage of these emissions in Europe.

Thus, green measures such as CBAM insure against ever-increasing carbon emissions from other nations by providing additional revenues from tax collection, which can further be used to invest in greener initiatives. This measure offers a competitive advantage for sustainable brands globally exporting to the EU. Older businesses have to resort to innovation such as using recycled fibers instead of new fibers, biodegradable fabrics, recycling and upcycling, circular fashion, 3D and virtual printing, self-cleaning clothes, rechargeable fabrics, waterless dying techniques, etc to add sustainability components to production processes. However, it is also important to note that sustainability is not a short journey, and hence businesses need to monitor it regularly to achieve sustainability goals.

Moreover, organisations can adapt to carbon accounting which will provide them with end-to-end calculations of carbon emissions in the development of their products while simultaneously tracking each node of the supply chain. Various carbon accounting software such as GreenStitch, etc, automatically calculates the emissions generated at various stages of the supply chain with internally developed formulae and algorithms. These calculations will identify the nodes with high carbon intensity and give focused solutions to reduce the same.

Further, with the increased responsible consumerism where sustainability is incorporated in making consumer choices, new business models can be discovered such as the sharing economy where renting and swapping of clothing reduces overall consumption; made-to-order business where a garment is made only when a customer has placed an order thereby reducing wastage; permanent collection business where a collection will fit across all seasons and clothing will last years; waste led design and upcycling models that use textiles waste to make new clothes.