Advancing Fashion's Climate Action with SBTi

Abstract

After adopting the Paris Agreement 2016, nations are taking various measures to achieve their Nationally Determined Criteria (NDCs) submitted to UNFCCC. These measures range from increasing the capacity of renewable energies to carbon taxation on imported goods and services. The nations have become strict in monitoring the carbon intensiveness of each production process and goods produced and imported into their economy. Thus, companies are now gearing up to set up their targets to make their production processes, and supply chains greener to survive in this changing landscape. SBTi, here, comes in handy as it is an end-to-end facilitating mechanism that helps to develop science-based targets aiming to make company’s processes sustainable and periodically monitors them for their timely achievement. This article dwells on why companies are adopting SBTs and details the criteria by SBTi required for setting up SBTs. It further explains in brief the how carbon accounting software such as GreenStitch and their experts can help in target setting, carbon accounting and ESG reporting.

In the Paris Agreement, national governments committed to limiting the global temperature below 2°C and pursuing efforts to limit temperature rise to 1.5°C, since temperatures beyond 2°C are linked to catastrophic climatic impacts and humanitarian crises. The increasing temperatures are due to increasing GHG emissions that are directly and indirectly linked to the corporate sector and industries. The textile industry contributes to 10% of the GHG global carbon emissions. This is accredited to the increasing trend of fast fashion and consumption. As researched by GreenStitch more than 70% of the GHG emissions come from upstream activities and remaining 30% are generated by downstream activities. Given the sectoral and business implications of the increasing GHG emissions in the value chains, business needs to mitigate the crisis. After recognizing the risks of climate change on their business growth and the opportunity it creates for innovation, the companies are setting goals to control global temperature. Still, their targets were not ambitious enough and inconsistent with the goal of 1.5°C. Hence, science-based targets (SBTs) are important to guide corporations in the right direction.

Science-based targets are the carbon emissions targets by the corporate sector, which align their climate mitigation strategies with the goals of the Paris Climate Agreement to limit global warming to 1.5°C above pre-industrial levels. These targets provide companies with clearly defined pathways to reduce Scope 1, 2 and 3 emissions. SBTs are grounded in an objective scientific evaluation of what is needed for global GHG emissions1 reduction determined by relevant carbon budgets, rather than what is achievable by any one company. They outline and advocate optimal strategies for reducing emissions and reaching net zero, offer methodologies and guidance for different sectors2 on how to set targets, and have a group of specialists and scientists who evaluate and validate the targets of the companies. Science-based targets initiative (SBTi), which started as a concept has now become a de facto standard for companies with more than 8000 companies and financial institutions registered with SBTi, and 5500 have validated science-based targets. Almost one-third of these target-setting companies are based in Asia. Sectoral analysis shows that there are more than 900 companies of textiles registered with SBTi.

SBTi offers sectoral guidance for companies, financial institutions, and SMEs separately for 14 sectors. Each guidance details approaches to set targets, sector-specific barriers in setting up targets, aims to increase consistency across companies’ targets in the sector, examples of good practices, and opportunities for collaboration. This step-by-step comprehensive guidance is prepared in line with the goals of the Paris Agreement. Not only do they aim to reduce the carbon emissions of each organization to achieve the 1.5 degree Celsius global temperature but also encourage them to work towards achieving the ultimate goal of reaching net zero by 2050 for which SBTI has specially developed a Net Zero Standard3. Further, the initiative is end-to-end facilitating the achievement of targets by periodic assessments. There is an independent assessment of each organization’s submitted targets to assess their realistic and achievable nature. Further, they also assess the progress of the organizations against the set targets annually and disclose this assessment for each company individually on their dashboard.

Why to set SBTi

Companies are increasingly adopting SBTs as part of a resilient business plan that drives ambitious climate action. Currently, more than 8000 companies are registered with SBTi with more than 3000 committing to Net Zero Standard after already setting up their targets. The number of companies joining SBTi has grown exponentially by almost 4 times in the last three years. The reasons companies are drawing towards this initiative are as follows:

Enhance organizational reputation: With the increasing responsible consumerism and widespread knowledge of the effects of consumer choices on the environment, sustainable lifestyle choices, and products are becoming a new norm. Thus, the company’s inclination towards developing eco-friendly products through green operations is of paramount importance. Setting targets with SBTi will enhance its reputation among consumers.

Resilience against regulations: Nations are gearing up to achieve their NDCs submitted in the Paris Agreement while bringing stringent carbon regulations to their economies. The European Union’s CBAM and the United States SEC are some regulations that have targeted carbon-intensive production. Thus, having science-based targets secures the companies against such stringent rules and makes them Paris Agreement-friendly.

Bolster investors’ confidence: According to the survey4 on investors’ interests and priorities found that 77% of investors reported being interested in sustainable investing among which 54% expect to increase the percentage of their portfolios allocated to sustainable investments within the next 12 months. Setting up SBTi targets will increase investor appeal and confidence in an organization while making an investment decision.

Increased innovations: Orderly transition to a low-carbon business model with the ultimate goal of achieving net zero opens up opportunities for innovation in the form of new and smart technology enablers. Companies can collaborate with new partners with a proven track record of developing new sustainable technologies or products. For instance, to reduce coal consumption, Indo Count Industries Ltd. installed a Back Pressure Turbine, Hot Water heat recovery system, and Auto Blow down at the boiler. This is in tandem with their strategy towards their SBTs.

Bottomline Cost savings: Many pioneers in adopting sustainable practices have already seen tangible cost savings and inturn increase profitability due to their environmental commitments. The increasing ability to operate efficiently and prepare for a future where non-renewable resources are scarce and costly is becoming crucial in ensuring sustained profitability rather than facing potential losses.

Provides competitive edge: A robust innovation framework, effective compliance mechanisms, strong brand recognition, and increased investor trust collectively give businesses a significant competitive advantage. These companies not only lead in their pursuit of Net Zero but also excel in seizing opportunities presented by the low-carbon economy, giving them a clear edge over their competitors.

Financing sustainably: Companies such as H&M, Adidas, Burberry, Chanel to name a few are raising funds through sustainability linked bonds and green bonds to decarbonise their supply chains. Such an initiative is in tandem with SBTi. This cost-effective capital acquisition have significantly improved the companies’ sustainability performance in terms of significant improvements in greenhouse gas (GHG) emissions. For instance, in 2023, Prada increased its procurement of electricity from certified renewable sources to 86%, a notable rise from 66% in 2022

How to set SBTi targets for the textile sector

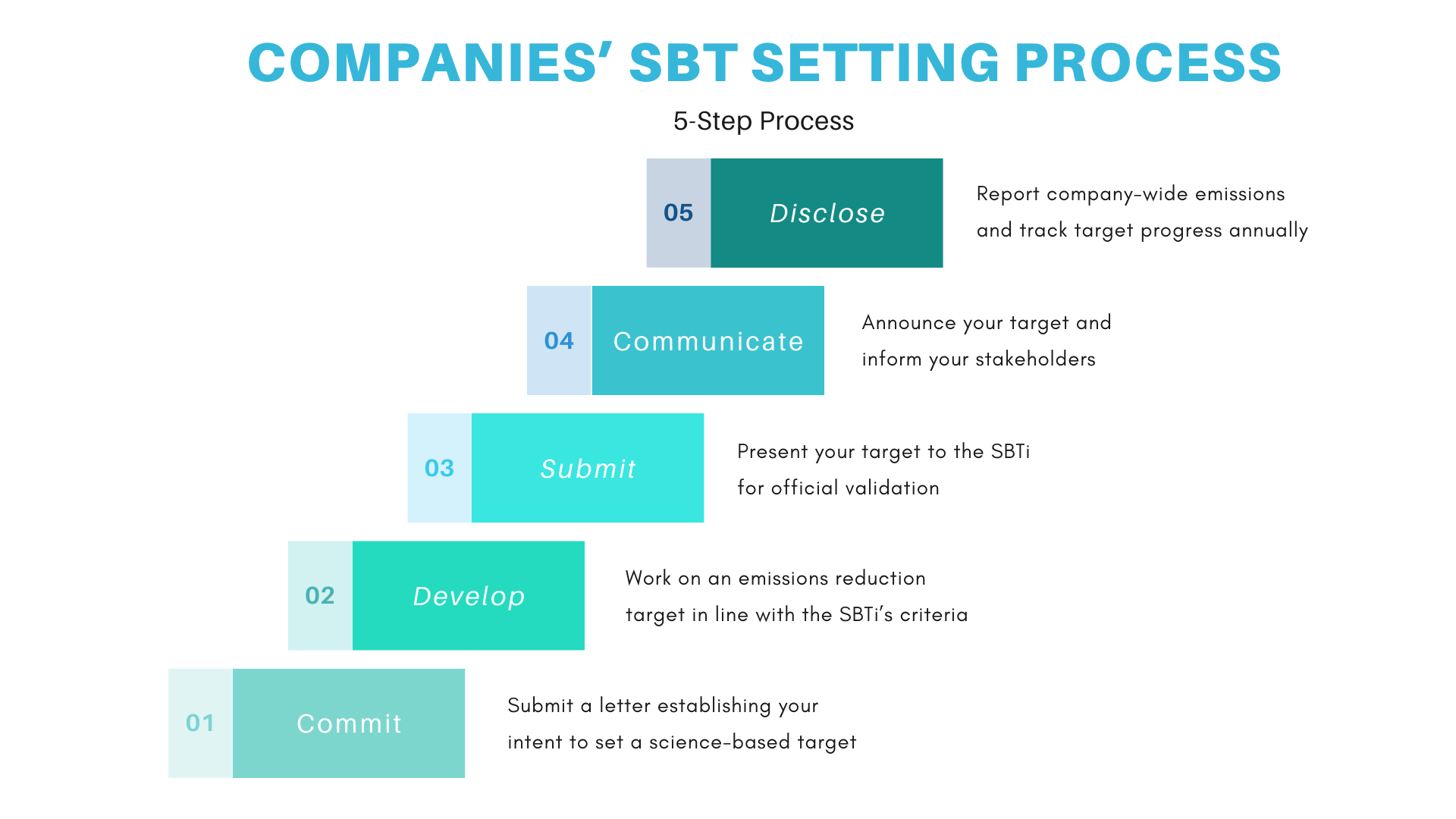

Science-based target initiative has separate mechanisms for setting up targets for (i) small and medium enterprises (SMEs), and (ii) large companies and financial institutions. For large companies, target setting is a five-step process which is depicted in the following figure where companies have to submit a letter of intent, work on establishing targets according to the sectoral decarbonization approach (SDA) of SBTi, present them to SBTi for validation, then announce it publicly within 6 months and lastly, companies have to annually disclose their emissions to SBTi for regular monitoring on the progress made for the achievement of targets.

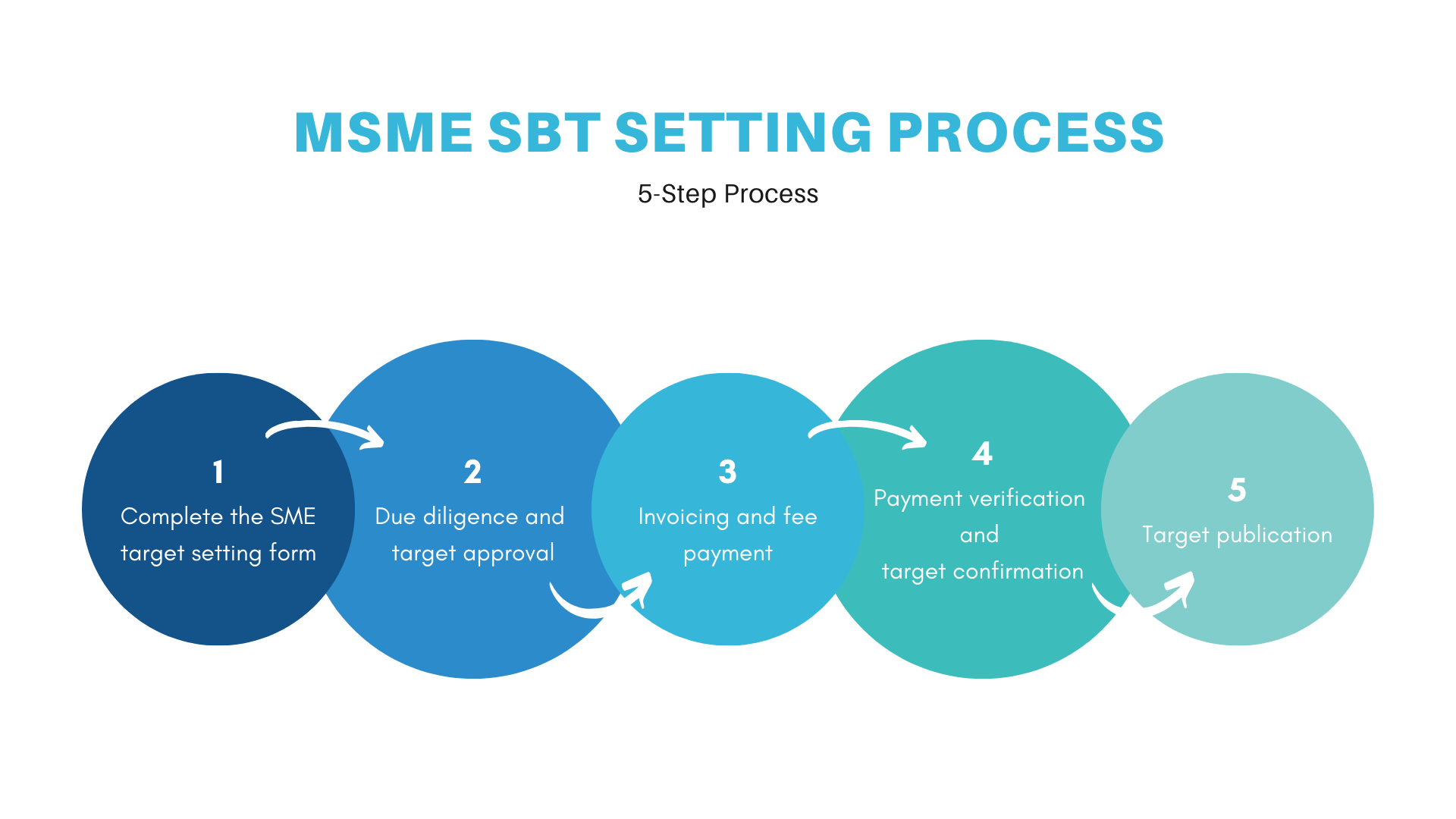

For MSMEs, the process is a little simpler, as it allows them to skip Step 1. They have to fill out an online application form asking for SME general information, Target Validation Service selection, requiring the selection of a service, a predefined target ambition related to base year choice, and the submission of the Company’s Emissions Profile with the relevant information (activities and emissions) per the GreenHouse Gas Protocol and Contractual and Payment information. After the submission of the form, due diligence will be done by SBTi after which the invoice will be sent to MSME for payment. After verification of payment and confirmation of targets, targets will be published on the SBTi website.

Setting up SBTis is a complex procedure, for which expertise from a third party such as Greenstitch, a fashion sustainability and “carbon accounting” AI software will be viable. The software helps in measuring “Scope 1, 2 and 3 emissions”, while simultaneously help in “fashion ESG reporting” of a company. Greenstitch understands the textile sector-specific criteria that are to be fulfilled for a target to be accepted as science-based during its assessment and thus prepare the company's sustainability reports as per the requirements of changing sustainability criterias and disclosures. These criteria are explained as follows:

- GHG emissions inventory: SBTi derives its conceptual definitions of “Scope 1, 2, and 3 emissions” from the GHG protocol corporate standard5 and directs to cover all the relevant emissions according to this standard. Companies may exclude 5% of the Scope 1 and 2 emissions combined in the boundary of the inventory and target. A few of the criteria specific to “Scope 1, 2, and 3 emissions” are:

- Scope 1 emissions: Include all the direct emissions from the combustion of biomass and biofuels. Further, it is voluntary to include emissions from land use and heat- and steam-related emissions.

- Scope 2 emissions: Targets to actively source renewable electricity are an acceptable alternative to scope 2 emission reduction targets. The SBTi has identified 80 percent renewable electricity procurement by 2025 and 100 percent by 2030 as thresholds.

- Scope 3 emissions: If scope 3 emissions are greater than 40% of the total emissions of the organization, then the organization must set scope 3 targets. Companies must set one or more emission reduction targets and/or supplier or customer engagement targets that collectively cover at least two-thirds of total Scope 3 emissions in conformance with the GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard. However, indirect-use phase targets6 would not be counted towards these 2/3rd of emissions.

- Disclose method for calculating emissions: SBTi makes it mandatory for companies to disclose the methods and emission factors used. For example, in the case of electricity in Scope 2, it is important to disclose whether a company followed a location-based or market-based approach to calculate base year emissions and to track performance against a science-based target.

- Time Frame: Targets must cover a minimum of 5 years and a maximum of 15 years from the date the target is submitted to the SBTi for official validation. The most recent year for which data are available should be chosen as the base year. If a company is developing long-term targets (covering more than 15 years) then mid-term targets are additionally required to be set. Lastly, the most recently completed GHG inventory must not be earlier than two years before the year of submission. It is also recommended to use the same base year for all long and mid-term targets to ensure consistency.

- Ambition: Ambition should be consistent with the decarbonization level to keep global temperature increase to well below 2°C and greater efforts should be made toward a 1.5°C trajectory. The combined Scope (1+2+3) is permitted where it is important for at least the Scope 1+2 portion must be in line with a well below 2°C scenario. However, offsets are not counted as an emission reduction toward the progress of companies' science-based targets.

- Recalculation and Validity: To ensure consistency with the most recent climate science and best practices, targets must be reviewed, and if necessary recalculated and revalidated following applicable criteria, at a minimum of every five years. The latest year in which companies with already approved targets must-revalidate is 2025. Further, if the company is experiencing significant adjustments such as changes in company structure, increase in the share of scope 3 (>40%), adjustments to base year inventory, etc, that could compromise relevance and consistency of the existing target, then targets are to be recalculated. The company has to notify the SBTi of any such changes taking place.

- Reporting: Companies are required to publicly report their company-wide GHG emissions inventory and progress against published targets on an annual basis in their annual report, sustainability report, or on their website. Further, they also have to publicly announce the approved targets by SBTi within six months of the approval date. If they cross this threshold of time, then targets will go through the approval process again.

After completing the above process, the various measures that companies can undertake to achieve the SBTs including shifting to lower GHG fuels, reducing the amount of carbon-intensive material in a product like using a few grams of cotton per t-shirt, replacing the material with a low GHG alternative such as using rPoly instead of virgin polyester, shifting material sourcing from higher carbon sources to lower ones, making supply chain investments such as installing renewable energy in factories, adopting sustainable packaging, etc. Carbon intensiveness in the supply chain of a company can be traced through Greenstich AI software which is helpful in mitigating the carbon hotspots in the operations.

Furthermore, companies need to prevent carbon emissions that result from the inputs purchased for production. They should engage with like-minded organizations that have either established or are in the process of setting their emission reduction targets. Participating in initiatives such as the CDP Supply Chain Program, which connects purchasing organizations with suppliers, enables suppliers to disclose their emissions using a standardized questionnaire. This approach aids in tracking carbon emissions throughout the supply chain and pinpointing areas that require action to mitigate emissions.

There are only 189 textile companies7 with approved SBTi targets. This low penetration of textile and apparel sector makes it important for textile companites irrespective of their size to adopt the expertise of a third party such as GreenStitch which can help in understanding their carbon footprint and in turn assist in setting up SBTs with SBTi. They also provides specialized services in “carbon accounting, “fashion ESG” reporting, “supply chain decarbonization”, “life cycle analysis” of products, and “traceability” of the carbon footprint of a product.

For more insights on how to set Science-based targets, reach out to us at narendra@greenstitch.io

References

- Science-based targets manual

- Guidance for different sectors on SBTi

- Net Zero Standard of SBTi

- Morgan Stanley Study 2024

- Definitions of Scope 1, 2 and 3 as per GHG Protocol Corporate Standard:

- Scope 1 emissions as Direct GHG emissions occur from sources that are owned or controlled by the company, for example, emissions from combustion in owned or controlled boilers, furnaces, vehicles, etc.; emissions from chemical production in owned or controlled process equipment excluding Direct CO2 emissions from the combustion of biomass and GHG emissions not covered by Kyoto Protocol such as CFCs, NOx, etc

- Scope 2 emissions account for GHG emissions from the generation of purchased electricity consumed by the company. Purchased electricity is defined as electricity that is purchased or otherwise brought into the organizational boundary of the company. Scope 2 emissions physically occur at the facility where electricity is generated.

- Scope 3 emissions are a consequence of the activities of the company but occur from sources not owned or controlled by the company. Some examples of scope 3 activities are extraction and production of purchased materials; transportation of purchased fuels; and use of sold products and services.

- Indirect use-phase targets are to influence the behavior of end users (e.g., education campaigns) or to drive the adoption of SBTs on corporate customers (e.g., customer engagement targets) are not required but are encouraged.

- SBTi Monitoring Report 2023